Enter the Era of the “Muni Credit Man”

As MainLine prepares its 2024 Outlook, we see a long-term trend in muniland that advisors and investors should start preparing for. MainLine sees changes coming in the municipal credit analysis process and Sleep Well At Night investing. Ranging from the economy, societal changes, politics, sector risks and preparing and managing for climate change risk, unprepared investors may find themselves sleeping with “one eye open”.

What a difference a few economic numbers can make in 30 days in the land of tax-exempts! MainLine has been calling for munis to outperform (and was wrong for over half the year), but that was all corrected in the last 30 days with a remarkable eyeopening performance. Munis posted their largest one-month performance in over 35 years, finally waking from a heavy sleep in never-never land.

Muni Market Review

The muni market posted its largest one month return since Volker conquered inflation in January of 1986. After a remarkable month, with munis up 6.35% versus US Treasuries at 3.47%, muni returns are now at a clip the coupon pace for the year at 3.98% versus US Treasuries at .67%.

November highlights were as follows:

- Muni yields were lower from 98 to 82 bps, with taxables lower by 58 to 48 bps.

- Out of favor 4% coupons and lower-rated spread sectors even participated, after big underperformance, as investors started chasing opportunities.

- Supply remains behind 2022 levels lower by 5.7%, but has been finishing strong. Estimates for 2024 and beyond have 2023 a low water mark for new issuance for years to come.

- Muni yield ratios are now considered rich versus taxables, but the long-end of the curve still represents relative value in muni land, as do out of favor sectors and coupons which have been trying to catch up.

MainLine will be hosting an investor call December 19th at 3:00 pm (EST). The meeting will focus on the performance of the Tax Advantaged Family of Funds, their outlook going forward, review of the muni market in 2023 and an overview of our outlook for 2024. We hope you can join us. If not, the call will be recorded and a link to the replay provided to all Fund investors.

Market News & Credit Update:

- With lots of news last month from local elections, the one that seems quite interesting in muni land was Texas residents voting that no entity in the State can levy a tax on the high net worth taxpayers. Although this is Texas, which is not considered “mainstream”, it does bring up an interesting debate between states on wealth distribution and public services. Some states are looking to pass taxes on the wealthy to help raise more revenue, provide more services and even out the big gap between the haves and have nots. Texas is looking to protect the wealthy, hoping economic activity will increase revenues and provide more fiscal freedom. It’s a long-term study on how this impacts population and wealth movements across the USA and ultimately credit quality of municipal issuers.

- Over the last two months MainLine has executed tax-loss swap trades for clients per their request. Losses were realized to offset any gains for the 2023 tax year or beyond and then proceeds reinvested at higher yields to increase their annual income. To date, MainLine has executed raising and reinvested over $16 million, realizing $2.2 million in losses while picking up $260,000 of annual income for clients. So, on average, for every $1 million sold, $138,000 in losses were realized and $45,000 in annual income was added.

- T+1 – The SEC has announced an important change to the standard securities settlement cycle. Effective May 28, 2024, most trades will settle one day after transaction, instead of the current two-day time period. Why? The SEC feels this will enhance investor protection by minimizing market value moves and risks associated with an extra day of volatility. What does this mean to you? Your muni bonds will settle next business day, instead of two business days.

Enter The Era of Muni Credit Man:

Introduction:

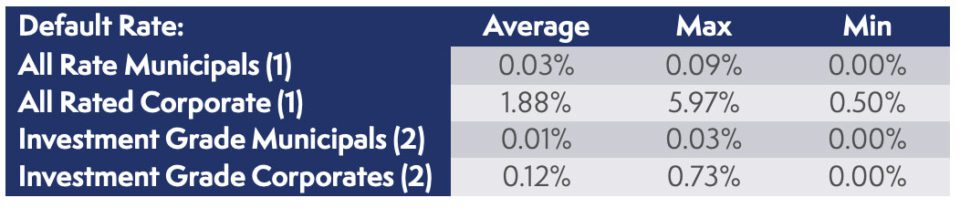

Municipal market investors have always assumed, and rightly so, their principal is protected. So much so that some buy bonds for projects and from issuers without a strong certainty that they can support their debt service and assume the state, or the authorities will find a way to make things work out and make them whole. As we have proudly shown so many times, the default rate for rated municipal bonds is near zero and the credit rating quality versus corporate bonds incomparable. A quick review the charts below show the annual default rates from 1986 to 2021 for all S&P rated corporate and municipal bonds and the credit rating profile of both as of 2021.

(2) All Bonds rated BBB- higher by S&P from 2000-2021

Investors without a lot of muni knowledge and conservative criteria, have been able to sleep well at night knowing munis for the most part are top tier quality. MainLine feels the era of sleeping well will require a little more work and muni expertise, as credit quality on average will decline and default rates increase for certain types of bonds.

Background:

As MainLine prepares its 2024 Outlook, there are several muni market trends that are catching our attention. One trend is that credit issues will become more of a focus. State revenues are slowing and budget tightening will need to offset this, but this is only the beginning and the typical economic cycle for state finances that municipalities have managed since the beginning of time. So why does MainLine think credit quality will weaken more than normal and default rates increase slowly over the next 30 years?

- Economic Cycle X2

- Societal Changes

- Sector Changes

- Preparing and managing Climate Change

- Polarized Politics

Municipal Credit Trends:

1) Economic Cycle X 2:

The end of several federal aid programs over the last three years will create fiscal cliffs and budget deficits especially in those states that cut taxes or used the proceeds to plug budget gaps. Add this to the decrease in state revenues from a potential economic slowdown and you have municipalities needing to find ways to bridge budget gaps. More bonds and the unpopular decisions to increase taxes and fees will test state budget discipline and ultimately increase debt levels going forward.

2) Changes in Society:

States are becoming less homogeneous and are prioritizing and expressing their opinions with policies and taxpayers money in different ways. What may be important in one state, may not be as important in another state. The blueprint for what a local government must provide to its residents and the strategy for demographic growth is becoming more defined state by state. This seems to be a trend that is just getting started and will grow. The focus needs to stay on “essential” service, those that are consistent from state to state.

As for demographic growth and change, some states are promising not to tax the wealthy, while others are planning to increase taxes on them. How does this impact population migration? Demand and costs of services?

Lastly, there seems to be an increase in the “what is mine is mine, what is yours you pay for” attitude when it comes to “for the public good” finance, This is reflected in the rise in metropolitan districts to build homes, the interference of states with property and casualty insurers and the unwillingness to pay any premiums not associated with risks nationally. Some states are even passing laws on who can and cannot do business in their states.

3) Climate Change: Direct/Indirect, Prepare/Incur

Climate change impacts on issuers both directly and indirectly, to prepare now, and to support later.

Direct Impact: The cost of climate change remains a moving target and it is a multipronged expense: the cost to prepare for it and the cost associated with it when there is a damage causing event. The need for infrastructure now to prepare is growing and remains unfocused and most states ill prepared. It is safe to assume a few things: states will be selling bonds to fund projects, some states more than others, some states will plan ahead, and some states will not.

Indirect Impact: An issuer may not have a lot of exposure to climate change, but could be indirectly impacted. For example, let’s assume NYC starts to be impacted due to rising water levels, and the state of New York needs to provide funds to help the City. These are funds that are now no longer available to the rest of the state, so poor Poughkeepsie can no longer rely on the state to help them with any aid due to a credit event. The State has chosen to support its big economic engine and not the small town. This is what we call “Muni Family Relationship Issues.”

4) Changes in Sector Risks:

There are changes coming due to the challenges above. A few sectors in the spotlight are as follows:

- Electric Utilities – The move to alternative fuels and clean energy could land some issuers with stranded assets due to a decrease in demand and a need to convert. This could increase costs, or for those who do not have the resources, go out of business. The ability to analyze electric utilities, and their risks has just become tougher.

- Healthcare/Hospital – The sector is finally recovering from COVID, with staffing levels slowly improving and operations getting back close to BC (before COVID). Yet, consolidating of health care systems to help control raising costs will increase competition and challenge management to integrate services. What will happen to the rural provider or the inner-city non-insured provider and how will they integrate and be supported? Healthcare is essential, but where it comes from and by who, is not.

- Moral/Limited General Obligation: As municipalities’ budgets become tight and its residents continue to watch out for themselves, how many projects that were deemed for the public good become expendable? The city has said they would support the project, but budget priorities and residents’ resistance to pay more taxes causes the city to walk away from the publicly financed ice rink, Water Park or new pickleball courts?

Moral pledges or financial backing based on need and not in law are not the same as unlimited and full faith and credit.

5) Polarized Political Risk:

Would a Governor pass a law or not support a city that is governed by a politician of a different party just to punish them for their beliefs and the residents who support them? Seems a bit extreme, but is it, given the polarity of beliefs and opinions these days? Compromise seems to be a sign of weakness and change a four-letter word.

Conclusion:

MainLine is not predicting the end of muni finance and sleep well at night investing. Default rates could double to .02% for investment rated issuers and still mean nothing (2 out of every 10,000 issuers). What we are saying is credit ratings will, on average, be lower and still represent toptier quality. This decline in overall credit quality will occur in certain types of bonds create a lot more credit “noise” and investor concerns which will be reflected in an increase of pricing volatility. The wrong type of bond can become very illiquid and discounted in price very quickly and impossible to sell.

MainLine feels there will be certain sectors, regions, and issuers that will be impacted to a greater degree. Muni credit analysis will require looking out further, such as longer time horizons, and beyond the issuer and to related “Muni family members.”

How to manage this growing risk in credit quality?

- Shorten your investment horizon with shorter term bonds, especially regarding climate change and in regions where this is a greater concern.

- Stay disciplined to diversification, by sector, by region, by parent, and by repayment dates.

- Increase credit risk profile. Stay with essential service, issuers with financial flexibility, proven management, good demographics, low political and climate risk profiles.

- I never thought I would say this, but it may be worth buying bonds backed by insurers such as BAM (Build America Mutual). If something goes wrong as an investor you have an extra layer of protection, but never buy a bond just because it is insured.

- Most important, seek muni advisory expertise, especially one that understands you want to Sleep Well At Night. Munis are not the exciting investment sector. Therefore, most advisors do not spend much time on them. They will regret this over the next 10 to 20 years.

Going forward, MainLine still believes you may have a better chance of getting hit by lightning than owning a defaulted muni bond. What we are warning is that certain bonds are more likely to get hit than others going forward based on history. MainLine wants to make sure our clients are not wearing a lightning rod on their head and not have to sleep with one eye open. – Enter Muni Credit Man.

View the Monthly Review PDF here – View November Report Chart